- Home

- Foreword

- Company portrait

- Strategy and Management

- Governance and Dialogue

- Product responsibility

- Employees

- Environment and Society

- GRI-Index

- Sites

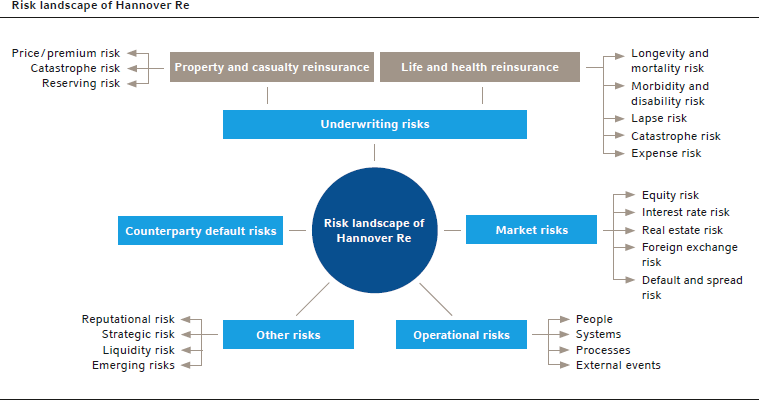

Risk landscape

In order to manage risks and ensure the company's economic stability on a lasting basis, it is essential to navigate through risks proactively and consider all relevant factors, whether they be economic, environmental or social in nature. Hannover Re's expertise in the appropriate assessment of risks is correspondingly sophisticated.

We make a fundamental distinction between risks that result from business operations of past years (reserve risk) and those stemming from activities in the current or future years.

Our risk landscape encompasses:

- underwriting risks in property & casualty and life & health reinsurance which originate from our business activities and manifest themselves inter alia in fluctuations in loss estimates as well as in unexpected catastrophes and changes in biometric factors such as mortality,

- market risks which arise in connection with our investments and also as a consequence of the valuation of sometimes long-term payment obligations associated with the technical account,

- counterparty default risks resulting from our diverse business relationships and payment obligations inter alia with clients and retrocessionaires,

- operational risks which may derive, for example, from deficient processes or systems and

- reputational risks, liquidity risks, strategic risks and emerging risks.

Just like other companies, we enter into some of these risks deliberately in the context of our business operations. Particularly for insurance undertakings, the acceptance and transformation of risk constitutes an essential part of business. The parameters and decisions of the Executive Board with respect to our company's risk appetite are fundamental to the assumption of such risks. They are based on calculations of the company's risk-bearing capacity. Through our business operations on all continents and the diversification between our Property & Casualty and Life & Health reinsurance business groups we are able to effectively allocate our capital in light of opportunity and risk considerations and generate a higher-than-average return on equity.

Operational risks, on the other hand, are never purposefully entered into – the emphasis here is on risk minimisation.

From a sustainability perspective, the (natural) catastrophe risk and the reputational risk are of particular relevance. Both are addressed in the context of our risk management. For example, the potential financial impacts of catastrophic events (including those caused by climate change) are continuously monitored. Furthermore, we are involved in several European industry associations and contribute to analyses and publications, especially in the area of emerging risks.

Emerging risks play a particularly important role for us. This is because the content of such risks cannot as yet be reliably assessed – especially on the underwriting side with respect to our treaty portfolio. Such risks evolve gradually from weak signals to unmistakable tendencies. It is therefore vital to detect these risks at an early stage and then determine their relevance. For the purpose of early detection of emerging risks we have had an efficient process in place for many years that spans divisions and lines of business and we have ensured its linkage to risk management. We report at length on emerging risks and their management in the chapter entitled "Product responsibility".

Strategies for dealing with the risks inherent in such perils are of the utmost importance to our company as a reinsurer. It is for this reason that our department specialising in the coverage of agricultural risks and the "Innovation Management" team work on products that can alleviate the financial impacts of climate change. In the context of our work in the Emerging Risks Initiative (ERI) of the CRO Forum, we are also investigating investment opportunities in so-called GreenTechs, which could increase our corporate contribution to CO2 reduction.

Group-wide risk communication and an open risk culture are important to our risk management. Regular global meetings attended by the actuarial units and risk management functions serve as a central anchor point for strategic considerations in relation to risk communication and risk culture. Furthermore, requirements for risk management are formulated in guidelines that are publicised throughout the company.